Global SSD Channel Market Contracts in 2024

- Global channel SSD shipments declined notably in 2024 as weak consumer demand and saturated notebook attach rates reshaped the market.

- TrendForce reports that consolidation accelerated, with the top brands strengthening their positions amid shifting supply dynamics.

- The outlook for 2025 suggests renewed momentum driven by AI-oriented devices and demand for higher-performance storage.

Market Conditions and Shipment Trends

Global SSD prices recovered during 2024 after hitting historic lows the previous year, and this shift reflected a gradual balancing of supply and demand. Retail segments nonetheless faced persistent headwinds as consumer electronics demand remained subdued. Notebook SSD penetration reached full saturation, which limited further shipment growth opportunities for module makers. TrendForce projects that total channel SSD shipments will reach roughly 101 million units this year, representing a 14% year-over-year decline.

Consolidation Among Leading Brands

Consolidation Among Leading Brands

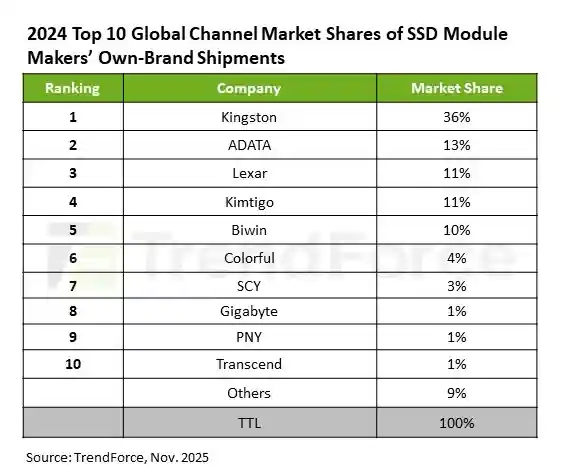

TrendForce’s ranking of SSD module makers shows that the market continued to consolidate, with the top five suppliers now holding more than 80% of total share. Kingston led the market once again with a 36% share supported by broad channel availability and stable product performance. ADATA followed at 13%, driven by its gaming-focused lineup and swift adoption of PCIe 4.0 and 5.0 products. Lexar secured third place with 11% share as it expanded its reach both in China and across international retail markets.

Movement Across Mid-Tier and Emerging Players

Kimtigo and Biwin claimed the fourth and fifth positions, separated only by narrow margins and benefiting from strong domestic demand alongside increasing overseas activity. Colorful maintained sixth place by leveraging its in-house controller and NAND capabilities to keep a competitive performance-to-price mix. SCY entered the top ten for the first time in seventh place, gaining visibility through broader penetration of Chinese retail channels. Gigabyte, PNY, and Transcend completed the ranking from eighth to tenth, each sustaining relevance through gaming influence, regional strength, or industrial specialization respectively.

Outlook for 2025 and Industry Implications

TrendForce expects AI-enabled PCs and edge devices to meaningfully shift storage requirements in the coming year. Higher-capacity and higher-performance SSDs are likely to see accelerated adoption as these workloads become mainstream. Module makers that refine their integration capabilities and strengthen channel strategies may benefit most in the next growth cycle. Competitive positioning will increasingly depend on aligning product portfolios with evolving performance demands rather than focusing solely on price competition.

Industry analysts note that client-side PCIe 5.0 adoption is progressing more slowly than early forecasts suggested, largely due to limited platform support and power-efficiency concerns. Despite this, manufacturers continue preparing next-generation drives as CPU and chipset roadmaps mature. Several vendors are also exploring more vertically integrated approaches to reduce reliance on external controller suppliers. These developments indicate that competition will likely intensify as technical differentiation gains importance across the SSD market.