Indian IT Firms Brace for Another Weak Quarter

- India’s top IT companies are expected to report another subdued quarter as weak U.S. demand and holiday‑season shutdowns continue to limit technology spending.

- Brokerages anticipate only modest revenue and profit growth, reflecting prolonged caution among global clients.

- Analysts say macroeconomic uncertainty, tariff concerns and shifting tech priorities are shaping the sector’s near‑term outlook.

Muted Growth Expected as U.S. Demand Softens

India’s major IT firms are preparing for another tepid earnings season, according to nine brokerages tracking the sector. Revenue for the top six companies is expected to grow around 4% year‑on‑year in the December quarter, with profits rising roughly 5%. These figures mark a slowdown from the 6.5% revenue growth reported in the September quarter. The industry has not seen double‑digit expansion since early 2023, when post‑pandemic digital transformation drove a surge in demand.

The broader $283 billion IT sector continues to face macroeconomic headwinds. Uncertainty around U.S. tariffs, proposed $100,000 visa fees and cautious client spending have weighed heavily on growth. India’s IT companies rely heavily on the U.S. market, making shifts in the world’s largest economy particularly impactful. Accenture’s recent earnings beat expectations due to AI‑related demand, but its unchanged outlook highlights ongoing caution.

Although India lacks pure‑play AI firms, domestic IT companies are beginning to shape AI strategies through acquisitions and partnerships. Brokerages expect AI‑driven demand to strengthen over the next six months. Growth may pick up into 2026 as clients resume larger transformation programs. For now, however, spending remains constrained by economic uncertainty.

Analysts say clients are hesitant to commit to major projects. Abhishek Pathak of Motilal Oswal Financial Services noted that macro and tariff concerns are prompting companies to delay incremental spending. This cautious stance has contributed to record foreign outflows from Indian IT stocks. Roughly $8.5 billion exited the sector in 2025, nearly half of all foreign withdrawals from Indian equities.

Market Performance Reflects Sector Weakness

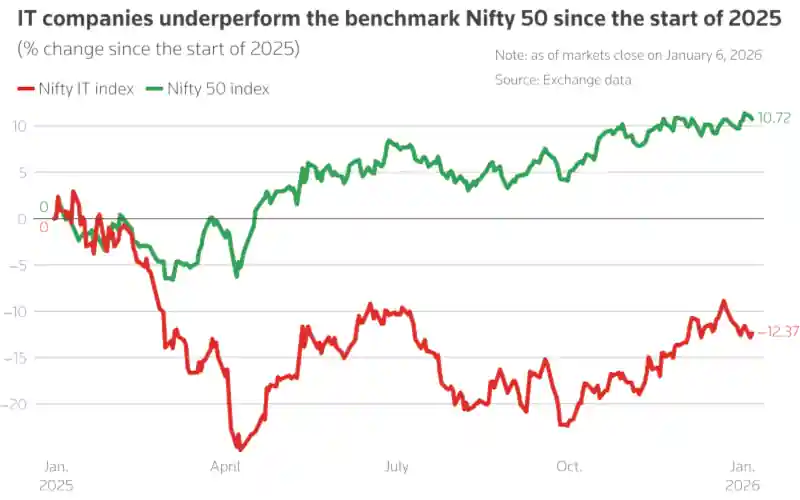

The Nifty IT index fell 12.6% in 2025, making it the worst‑performing sector in India. Markets across Asia and other emerging economies outpaced Indian IT stocks during the year. Investors have been discouraged by weak spending trends and persistent uncertainty in key markets. These pressures have created a challenging environment for companies heading into the new earnings cycle.

Tata Consultancy Services will open the reporting season on January 12. Its revenue is expected to rise about 4.2% year‑on‑year, slower than the 5.6% growth recorded last year. Infosys and HCLTech are forecast to post revenue growth of 8.1% and 4.6%, respectively. These figures represent only slight improvements over the previous year’s performance.

Most brokerages do not expect HCLTech to revise its fiscal 2026 revenue forecast of 2%–3%. Infosys is also unlikely to raise its guidance of 3%–5%. These conservative projections reflect the sector’s cautious outlook. Companies are preparing for continued margin pressure as wage hikes and furloughs affect profitability.

Fewer working days in the December quarter due to global holidays further weigh on billing and revenue. Brokerages warn that this seasonal slowdown will remain a structural challenge for IT firms. Despite these pressures, some segments show signs of resilience. The BFSI sector, in particular, continues to support deal activity.

AI Momentum and Sector Tailwinds Could Aid Recovery

Analysts see potential for improvement by mid‑2026. Deal ramp‑ups, early AI strategy formation and rupee depreciation may provide support in the coming quarters. Companies are increasingly integrating AI into their service offerings, which could help offset slower demand in traditional outsourcing. These shifts may gradually reshape the sector’s growth trajectory.

The BFSI segment remains a bright spot for Indian IT firms. Financial institutions continue to invest in modernization and regulatory compliance, creating steady demand. This resilience may help cushion the impact of weaker spending in other industries. Brokerages believe BFSI strength will play a key role in stabilizing overall performance.

Policy easing, tax cuts and stable domestic growth are expected to boost earnings across Indian equities in the December quarter. However, IT firms remain structurally weaker due to their global exposure. The sector’s recovery will depend heavily on improvements in U.S. economic sentiment. Until then, companies are likely to maintain conservative forecasts.

Indian IT firms are navigating a complex environment shaped by global uncertainty and shifting technology priorities. AI adoption offers long‑term opportunities, but near‑term challenges persist. Brokerages expect gradual improvement rather than a rapid rebound. The next few quarters will be critical in determining how quickly the sector can regain momentum.

India’s IT sector has historically been one of the most reliable performers in the country’s stock market, but 2025 marked its worst year in over a decade. Analysts note that the last comparable downturn occurred during the global financial crisis, when U.S. spending cuts similarly disrupted outsourcing demand. This parallel underscores how closely the sector’s fortunes remain tied to the health of the U.S. economy.